题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[单选题]

According to STCW Code, which is not a level of responsibility on board a ship()

A.Master level

B.Management level

C.Operational level

D.Support level

答案

答案

A、Master level

如果结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

如果结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

A.Master level

B.Management level

C.Operational level

D.Support level

答案

A、Master level

如果结果不匹配,请 联系老师 获取答案

更多“According to STCW Code, which …”相关的问题

更多“According to STCW Code, which …”相关的问题

A.the master

B.the officer in charge of watch

C.the company

D.the Administration

A.move with agility

B.step over coamings

C.climb up and down vertical ladders

D.lift,pull, push and carry a load

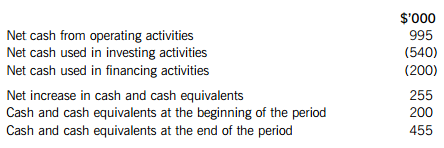

An extract from the statement of cash flows for the year ended 31 December 20X7 for Top Trades Co is presented as follows:

Which of the following statements is correct according to the extract of Top Trades Co’s statement of cash flows?

A.The company has good working capital management

B.Net cash generated from financing activities has been used to fund the additions to non-current assets

C.Net cash generated from operating activities has been used to fund the additions to non-current assets

D.Existing non-current assets have been sold to cover the cost of the additions to non-current assets

Which of the following statements describes target costing?

A.It calculates the expected cost of a product and then adds a margin to it to arrive at the target selling price

B.It allocates overhead costs to products by collecting the costs into pools and sharing them out according to each product’s usage of the cost driving activity

C.It identifies the market price of a product and then subtracts a desired profit margin to arrive at the target cost

D.It identifies different markets for a product and then sells that same product at different prices in each market

Jackdaw Motor Cars Co (Jackdaw) manufactures a range of motor cars and its year end is 31 January 2015. You are the audit supervisor of Puffin & Co and are currently preparing the audit programmes for the year-end audit of Jackdaw. You have had a meeting with your audit manager and he has notified you of a number of issues identified during the audit risk assessment process.

Land and buildings

Jackdaw have a policy of revaluing land and buildings, this is undertaken on a rolling basis over a five-year period. During the year Jackdaw requested an external valuer to revalue a number of properties, including a warehouse purchased in May 2014. Depreciation is charged on a pro rata basis.

Work in progress

Jackdaw undertakes continuous production of cars, 24 hours a day, seven days a week. An inventory count is to be undertaken at the year end and Puffin & Co will attend. You are responsible for the audit of work in progress (WIP) and will be part of the team attending the count as well as the final audit. WIP constitutes the partly assembled cars at the year end and this balance is likely to be material. Jackdaw values WIP according to percentage of completion, and standard costs are then applied to these percentages.

Required:

(a) Explain the factors Puffin & Co should consider when placing reliance on the work of the independent valuer. (5 marks)

(b) Describe the substantive procedures the auditor should perform. to obtain sufficient and appropriate audit evidence in relation to:

(i) The revaluation of land and buildings and the recently purchased warehouse; and (6 marks)

(ii) The valuation of work in progress. (4 marks)

(c) During the audit, your team has identified an error in the valuation of work in progress, as a number of the assumptions contain out of date information. The directors of Jackdaw have indicated that they do not wish to amend the financial statements.

Required:

Explain the steps Puffin & Co should now take and the impact on the audit report in relation to the directors’ refusal to amend the financial statements. (5 marks)

A.1995年的STCW公约附则修正案和STCW规则已于1998年8月1日起强制执行

B.1995年的STCW公约附则修正案和STCW规则已于1997年2月1日起强制执行

C.1995年的STCW公约附则修正案和STCW规则已于2002年2月1日起强制执行

D.1995年的STCW公约附则修正案和STCW规则已于1998年8月1日起生效

A.STCW公约安特卫普修正案

B.STCW公约马尼拉修正案

C.STCW公约东京修正案

D.STCW公约鹿特丹修正案

The following scenario relates to questions 6–10.

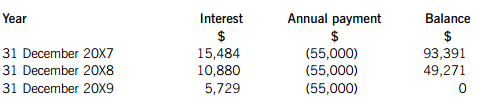

On 1 January 20X5, Blocks Co entered into new lease agreements as follows:

Agreement one This finance lease relates to a new piece of machinery. The fair value of the machine is $220,000. The agreement requires Blocks Co to pay a deposit of $20,000 on 1 January 20X5 followed by five equal annual instalments of $55,000, starting on 31 December 20X5. The implicit rate of interest is 11·65%.

Agreement two This three-year operating lease relates to a fleet of vans. The fair value of the vans is $120,000 and they have an estimated useful life of five years. The agreement requires Blocks Co to make no payment in year one and $48,000 in years two and three.

Agreement three This sale and leaseback relates to a cutting machine purchased by Blocks Co on 1 January 20X4 for $300,000. The carrying amount of the machine as at 31 December 20X4 was $250,000. On 1 January 20X5, it was sold to Cogs Co for $370,000 and Blocks Co will lease the machine back for five years, the remainder of its useful life, at $80,000 per annum.

According to IAS 17 Leases, which of the following is generally considered to be a characteristic of an operating, rather than a finance, lease?

A.Ownership of the assets is passed to the lessee by the end of the lease term

B.The lessor is responsible for the general maintenance and repair of the assets

C.The present value of the lease payments is approximately equal to the fair value of the asset

D.The lease term is for a major part of the useful life of the asset

For agreement one, what is the finance cost charged to profit or loss for the year ended 31 December 20X6?

A.$23,300

B.$12,451

C.$19,607

D.$16,891

The following calculations have been prepared for agreement one: How will the finance lease obligation be shown in the statement of financial position as at 31 December 20X7?

A.$44,120 as a non-current liability and $49,271 as a current liability

B.$49,271 as a non-current liability and $44,120 as a current liability

C.$93,391 as a non-current liability

D.$93,391 as a current liability

For agreement three, what profit should be recognised for the year ended 31 December 20X5 as a result of the sale and leaseback?A.$24,000

B.$120,000

C.$70,000

D.$20,000

For agreement two, what would be the correct statement of profit or loss entries for the year ended 31 December 20X5?A.Depreciation of $24,000 and no lease rental expense

B.No depreciation and lease rental expense of $32,000

C.Depreciation of $24,000 and lease rental expense of $32,000

D.No depreciation and lease rental expense of $48,000

请帮忙给出每个问题的正确答案和分析,谢谢!

A.Ⅰ+Ⅱ+Ⅳ

B.Ⅰ+Ⅲ+Ⅳ

C.Ⅱ+Ⅲ+Ⅳ

D.Ⅰ+Ⅱ+Ⅲ

A.①②③

B.①②⑤

C.②③④

D.②④⑤